in  Newsletter

Newsletter

Newsletter

Bluebook-at-a-glance

Increased — 12

Decreased — 366

Stable — 419

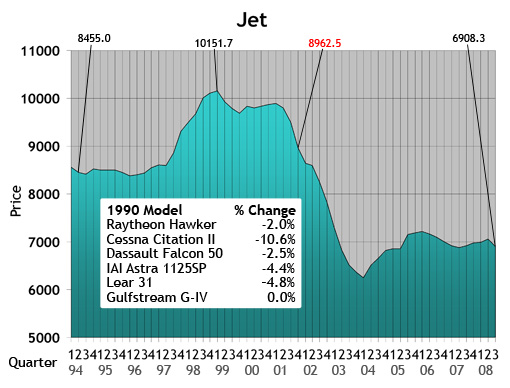

Values of a few model groups did increase. The Dassault Falcon 7X, Bombardier Challenger 604 and 605 as well as the Gulfstream G150 all experienced increases in value. All of the other models remained unchanged or experienced reductions in the reported average retail values. Prices of late-model, long-range, large-cabin models generally remained stable during this reporting period. One noted exception is the Falcon 50 series, which was down $250,000-$500,000 when compared to the previous quarter.

The Cessna Citation X also demonstrated lower values. Extra value can be added to a Citation X if the engines are enrolled in Rolls Royce CorporateCare. For other late-model, mid-range, cabin-class jets, such as the Cessna Citation 560 series, Hawker 800XP and Lear 45XR, values were unchanged for yet another quarter. Late-model light jets, such as the Cessna 525 CJ, and Hawker 400XP were down in value when compared to the previous quarter. For the most part, earlier-model jets were down. This segment will probably not see any future appreciation in values.

Bluebook-at-a-glance

Increased — 30

Decreased — 309

Stable — 277

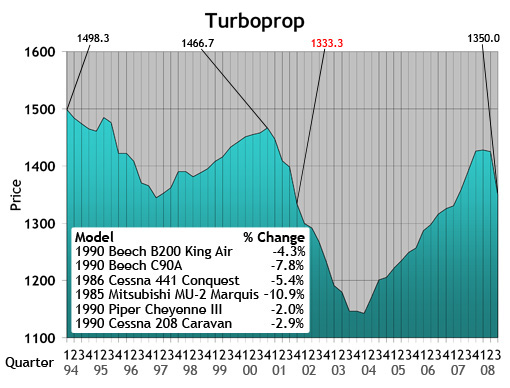

AMSTAT reports that inventories of pre-owned turboprop aircraft listed for sale or lease and covered in Aircraft Bluebook grew by 1 percent. But overall, less than 9 percent of the total turboprop fleet tracked by Bluebook was on the offering table. Sales were average with values holding steady or slightly lower than the previous quarter.

Cessna Caravans were reported down an average of $25,000. The Cessna Conquest and DeHavilland Twin Otter were down $100,000. Fifteen-year-old King Air 90s dropped $100,000 while later models remained unchanged. Most of the King Air 350 and 200 markets had little or no change in values from the previous quarter. Late-model Pilatus PC-12s experienced modest gains. The Socata TBM 700 series remained stable.

Bluebook-at-a-glance

Increased — 0

Decreased — 509

Stable — 159

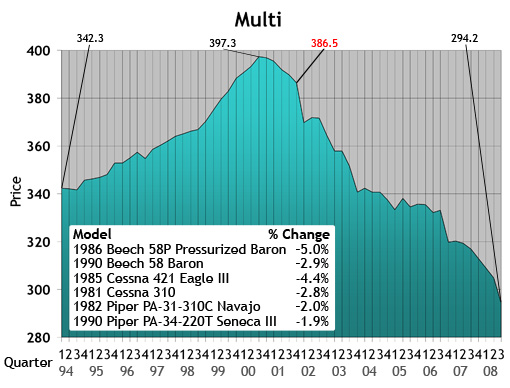

Well-equipped and maintained twin-piston aircraft are selling. Other piston-twins that are in need of maintenance and upgrades are taking more than 6 months on market to sell at discounted prices.

Beech Barons were generally down $10,000 when compared to the previous quarter. Values of pressurized Cessna twins also fell $10,000. Earlier-model piston-twin prices also dropped an average of $5000 from last quarter.

Bluebook-at-a-glance

Increased — 184

Decreased — 1327

Stable — 897

No surprises in this segment. Like the piston-twin market, well-equipped and maintained singles continue to move, though evidence of lower values was evident when compared to the previous quarter. Activity was as scattered as a midday summer storm. Some dealers reported a noticeable lack of activity while others reported business as usual. Surprisingly, piston ag planes experienced some modest gains. Tail-draggers also demonstrated gains in value. The Cessna 185 and Piper Cub had modest increases in values when compared to last quarter. Cirrus, late-model Beechcraft, Piper and Mooney all experienced reductions in value in the single-piston category.

Bluebook-at-a-glance

Increased — 39

Decreased — 68

Stable — 835

Helicopter values remained consistent during the second quarter of 2008. Days on market continue to be limited for well-equipped, late-model helicopters. Values predominantly remain unchanged for the third quarter of 2008 as noted in the fall 2008 edition of Bluebook.

Please visit us if you are attending Jet Expo in Moscow, Russia, Sept. 17-19. We will be located with AC-U-KWIK in booth No. 136. At NBAA, Oct. 6-8 in Orlando, Fla., stop by and visit us. We are located in booth 1663. If you plan to attend MEBA in Dubai, UAE, Nov. 16-18, our booth number is 334. We look forward to visiting with you.

Newsletter

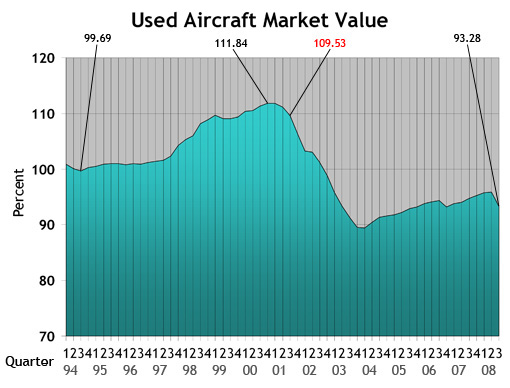

Used Aircraft Market: This chart displays each model's quarterly value in relationship to its average equipped price at the inception of the aircraft. The study begins in the spring quarter of 1994 and includes the Jet, Turboprop, Multi, Piston and Helicopter. For all charts, the red number indicates the first reporting date after 9-11.

Jet: The jet chart depicts the average price (in thousands) of the six 1990s jets listed in the box.

Turboprop: The turboprop chart depicts the average price (in thousands) of a 1985, 1986 and four 1990 turboprops listed in the box.

Multi: The multi chart depicts the average price (in thousands) of the six multi models listed in the box. Each model’s year will precede the name of the aircraft.

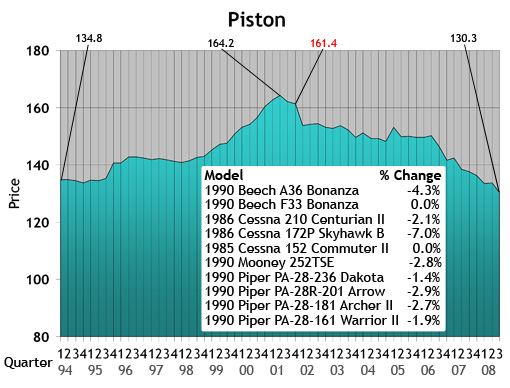

Piston: The piston chart depicts the average price (in thousands) of the 10 pistons listed in the box. Each model’s year will precede the name of the aircraft.

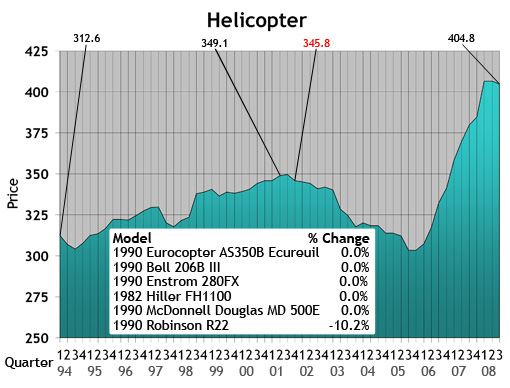

Helicopter: The helicopter chart depicts the average price (in thousands) of the six helicopters listed in the box. Each model’s year will precede the name of the aircraft.

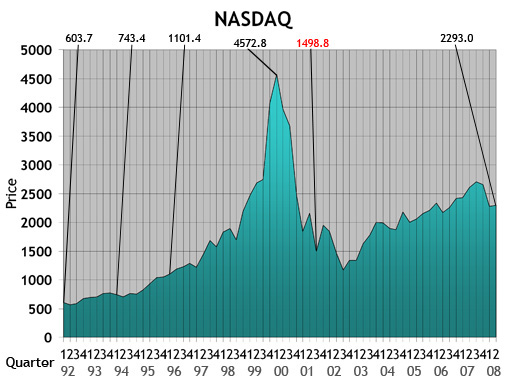

NASDAQ: This ratio scale chart depicts the change for the NASDAQ daily average from quarter to quarter beginning at the end of the first quarter of 1992. Each data point represents the closing daily average on the last trading day of each quarter. This study originates in the first quarter of 1971.

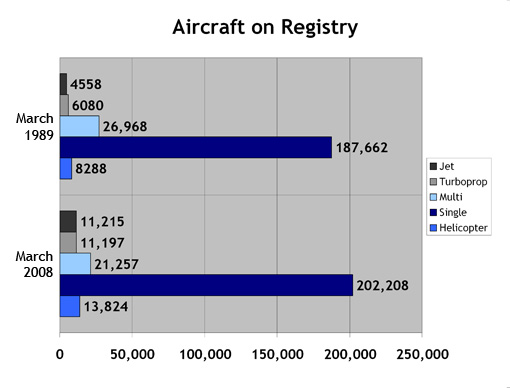

Aircraft on Registry: The Aircraft on Registry chart depicts the number of aircraft reported in Aircraft Bluebook that are listed on FAA records and considered to be in the U.S. inventory.

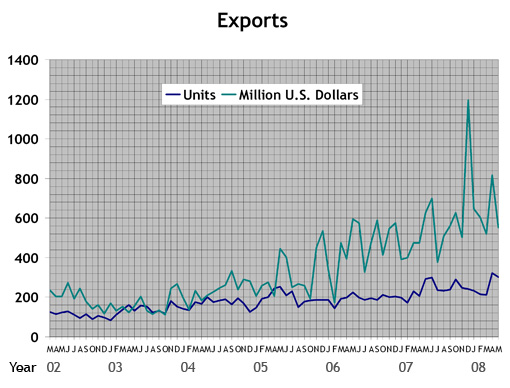

Export Data: These numbers include both airplanes and helicopters. The numbers do not include aircraft that have empty weights in excess of 33,069 lbs.

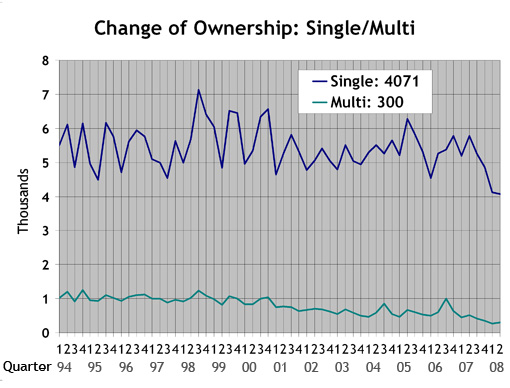

Single/Multi: The blue line in the Single/Multi chart depicts change-of-ownership data for singles. The green line represents multis.

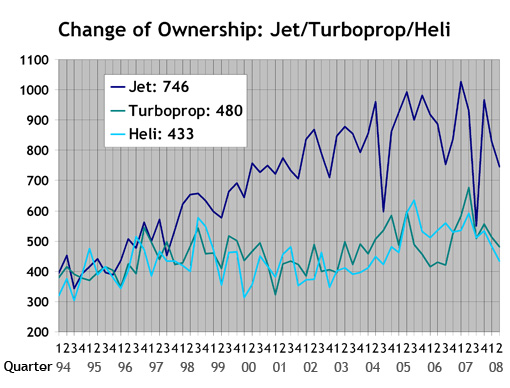

Jet/Turboprop/Heli: The dark blue line in the Jet/Turboprop/Heli chart represents change-of-ownership information for jets. The green line depicts turboprops, and the light blue line represents helicopters.

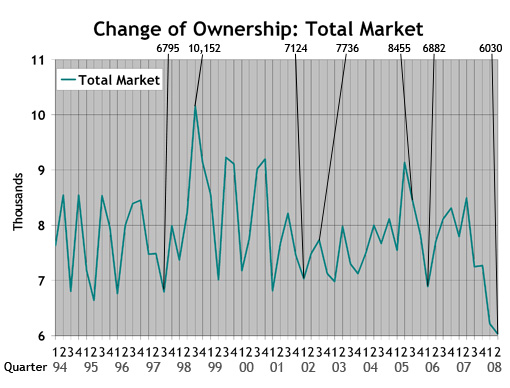

Total Market: Depicts change-of-ownership data for all aircraft included in the Aircraft Bluebook. The numbers are from the FAA Registry. Gliders, homebuilts, airliners and other aircraft not found in the Bluebook are not included in this study.

Charts